Pricing strategy changes across the technology life cycle

Steven Forth is CEO/Co-founder at Ibbaka

Pricing has important transition points across the technology adoption cycle. How you think about value and use it to shape your pricing strategy changes as your buyer’s motivation changes. It is critical that leadership, investors, product and services managers, and marketing understand these transitions and be honest about where a product or technology actually is in the life cycle.

We frequently see companies in bowling alley markets pricing as if they are already in a tornado. This is a recipe for failure. On the other hand, failing to evolve your pricing strategy and value selling definition when a tornado develops can cause a company to stall out and cede the market to a more nimble competitor. Again, as the tornado matures and the market moves to the late majority (which is the vast majority of products and revenues today), another transition is needed. Understanding how to sell value at each stage is essential for long-term success.

An example of this is the SaaS market for Client Relationship Management systems (CRMs). When Salesforce.com was introduced, it had a simple value proposition: sales leaders could adopt it quickly and control it without depending on the IT function. As CRMs moved into the bowling alley, functionality and value drivers expanded and became more focused on specific business problems, revenue predictability, and salesforce management. Then something happened. Almost every CEO came to the conclusion that they deserved a CRM. And they got one. Value drivers became as generic as possible, as did Salesforce’s marketing messages. Today, CRM is a late majority market, with industry solutions like Veeva for the life sciences beginning to eat away at Salesforce. This evolution is a classic value selling example-showing how selling value shifts from unique differentiation to broad-based adoption and, eventually, to added value selling in niche markets.

Value drivers, and following them, pricing and willingness to pay (WTP), go through transitions as an offer moves from early adopter, to bowling alley, to tornado, to late majority. Pushing for horizontal value drivers and a mass market too early, or staying with them too long, is a recipe for failure. Investors should make sure they are not encouraging this behavior, and that pricing strategies always reflect the value of sales at each stage.

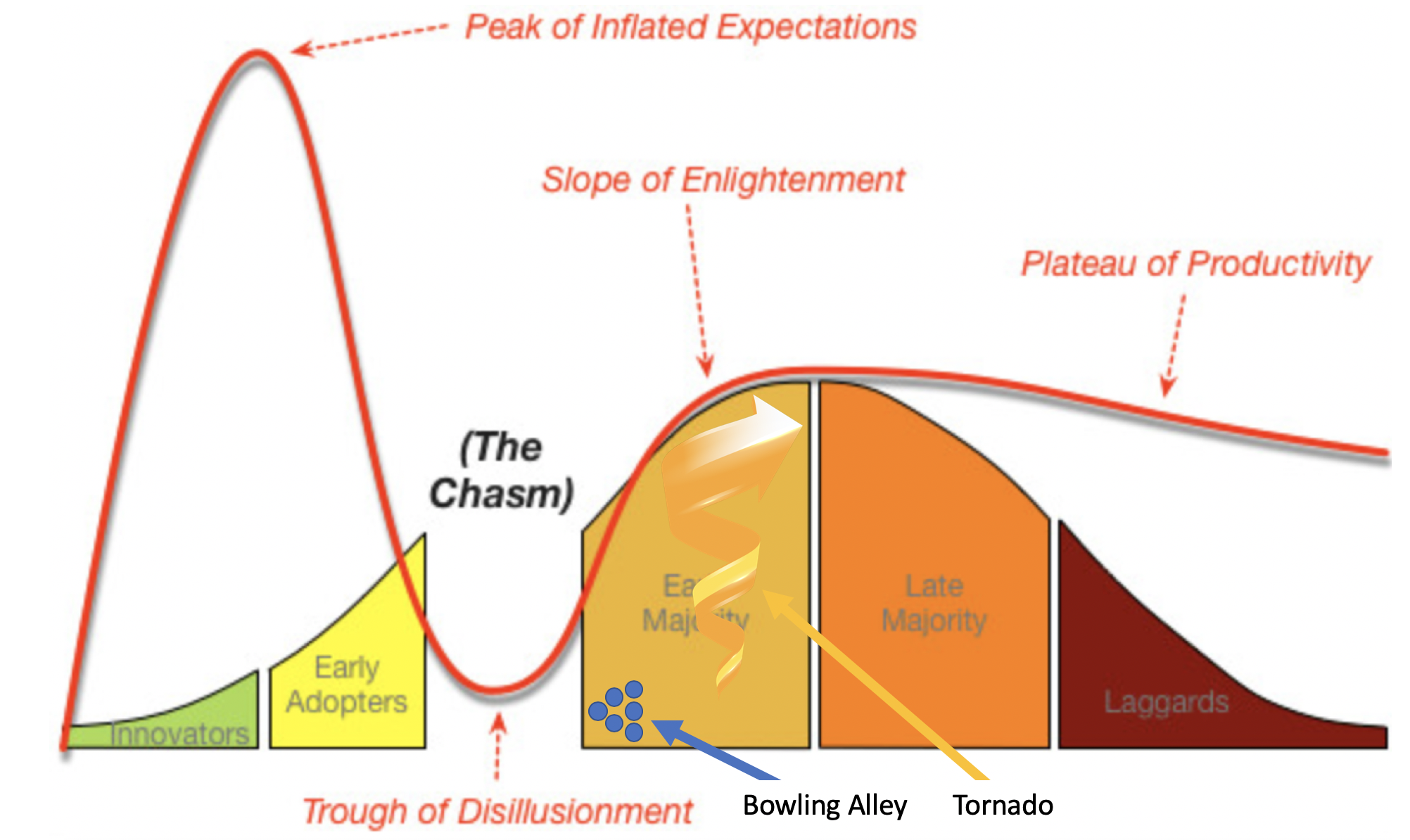

One way to frame this is using Geoffrey Moore’s technology adoption cycle. You know, the one that goes from innovators, to early adopters, from highly targeted bowling alley markets to the tornado (occasionally), and on to the maturity. In this post, we are concerned with the early part of the cycle, up to and including the tornado.

I like this version of the standard technology lifecycle graph as it layers in the Gartner technology hype cycle. The mapping is not perfect, but it is suggestive, so it is useful to take a look at Gartner’s current hype cycle as a way to make a first pass at where different technologies may be on the technology adoption cycle. Gartner publishes hype cycles for many sectors, so search their site for those that best represent your own business. The 2018 hype cycle for the digital workplace is shown below.

Hype Cycle for the Digital Workplace, 2018

It is easy to misunderstand the hype cycle. The assumption is that technologies early in the cycle are somehow unsubstantial or unproven. This is not usually true. They generally represent powerful technology innovations that are looking for commercial applications. Which brings us back to the technology adoption cycle.

The key thing to remember about technology adoption is that the buyer’s reasons for buying change across the lifecycle. As the reasons to buy change, so do the value drivers that matter and the customer’s willingness to pay. This is why a value-based conversation is critical at every stage, ensuring your pricing and value messaging align with what matters most to your target segments.

Pricing for Innovators

Innovators are buying because something is new, and they are not all that concerned with the business value. They tend to have a very low willingness to pay (WTP) and are not moved by economic arguments. By the time a technology has reached the peak of inflated expectations, they have often moved on. At this stage, value selling definition is less relevant, as these buyers are motivated by novelty rather than ROI or business outcomes.

Pricing for Early Adopters

Early adopters are buying to get a unique competitive advantage. They are looking for a singular set of value drivers that apply only to them. Value drivers with broad appeal are not relevant to what they are trying to achieve. You generally have to know an early adopter’s business well to win them over, and tailor the solution to their unique needs. Early adopters tend to have a very high willingness to pay as they are buying for competitive advantage. Here, business value selling and value-based conversations are essential, as you must demonstrate how your solution delivers differentiated value for their specific goals.

Pricing for Bowling Alley Buyers

Bowling alley buyers are buying to stay competitive in their own market. They care most about their direct competitors and will buy if they see their competitors buying. They respond to value drivers that are directly applicable to the mechanics of their own business. Willingness to pay is constrained by the economics of the business and is generally much lower than for early adopters. In an odd way, willingness to pay tracks the hype cycle! Selling on value in this context means clearly articulating how your solution addresses their operational challenges and delivers measurable outcomes.

Pricing for Tornado Buyers

Tornado buyers see the solution as a cost of doing business. As it is a cost, they are even more price sensitive than bowling alley buyers, but there are a lot more of them. Failing to flip from vertical to horizontal value drivers and adjusting pricing accordingly is one of the main reasons companies get left out of tornado markets. Remember, only a few companies survive the transition from bowling alley to tornado. Most companies are acquired, go out of business, or are forced to change business models. At this stage, added value selling and clear value selling examples can help differentiate your offer in a crowded market.

Pricing for the Late Majority

Late majority buyers tend to have a good understanding of the value of a solution. The value drivers are known, tested, and approved. The tornado winners often falter here, leaving openings for a new generation of innovators who develop targeted solutions for specific markets. The successful tornado companies stay with the horizontal business models that have brought them so much success and discount the targeted solutions. Over time, the late majority market diversifies, and many new niches appear. The large incumbents see their once dominant position slip away. This seems to be happening to Oracle and SAP. One can even see early signs of Salesforce struggling to compete on many different fronts. The good news, though, is that willingness to pay tends to rise steadily as focused solutions create more and more differentiated value. This is where how to build value in sales and what is value-based selling become crucial for maintaining pricing power and customer loyalty.

Summary

Pricing coaches and strategists need good early warning systems to help them predict when a market will go through transition points. Moving too early to horizontal value drivers that appeal to the widest market possible can cause a company to stall out and reduce its pricing power. Making the switch to horizontal value drivers and resetting prices too late leaves the door open to competitors. Failing to move back to vertical value drivers focused on differentiation lets other companies exploit the steadily increasing willingness to pay available to differentiated solutions.

Throughout the technology adoption lifecycle, successful pricing relies on understanding value selling definition, engaging in value-based conversations, and continuously building value in sales.

Originally published on June 3rd, 2019. Updated on May 14th, 2025.